USF doing the right thing with student loans

In 2016, USF was found to have the lowest rate of defaulted loans among universities and colleges in Tampa Bay, according to a study from the financial products comparison company LendEDU.

Defaulting on student loans occurs when alumni violate the agreed upon repayment plan. For most federal student loans, this occurs when a loan payment is late for more than 270 days.

The statistic is an excellent indicator for USF student success and is much better than the average public college default rate in the U.S. as well as for-profit universities. “For-profit” means that the school operates as a corporation and are often beholden to shareholders.

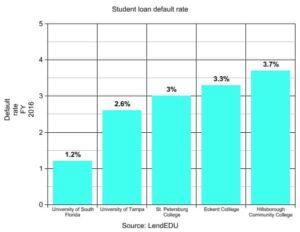

USF was found to have a 1.2 percent student loan default rate, which is No. 239 for lowest rate in the nation and No. 8 for lowest in Florida, according to LendEDU.

The rate is a good indicator of whether a degree received from an educational institution truly helped a student get a job that paid them enough to keep up with their student loan repayments.

The same study found that the national average default rate for the U.S. was 10.1 percent and Florida’s average was 7.33 percent. This means that students at USF are significantly less likely to be in a position where they cannot make their student loan payments.

USF has this ranking because of the affordability of our school without sacrificing the quality of education received.

Specifically, other Tampa Bay universities have higher rates of defaulted loans than USF. University of Tampa has a default rate of 2.6 percent and St. Petersburg College has a default rate of 3 percent, according to LendEDU. However, all of these rates in the area are still much lower than the national average.

At a time of increasing student debt, prospective students need to consider whether there is a high probability of not being able to financially “keep up.” Fifty-two percent of students take out student loans at USF compared to the national average of 69 percent, according to University Scholarships and Financial Aid Services.

The average amount of debt taken out by a USF student is $21,565, which is significantly less than the national average of $29,800.

The same study from LendEDU, which uses data from the Department of Education, highlighted some of the themes that contribute to an increased rate of students defaulting on their loans.

For instance, the best indicators of a high default rate was whether an institution was for-profit. The study found that for-profit colleges and universities had an average default rate of 15.2 percent, public colleges and universities had an average default rate of 9.6 percent and nonprofit private schools had a default rate of 6.6 percent.

There are many lists that highlight USF’s achievements, but this study about defaulting loans from LendEDU is a particularly good illustration of USF’s history of leading students debt free.

Jared Sellick is a junior majoring in political science.

More Stories

OPINION: Hey USF, stop swiping on Tinder and start making real connections.

Let’s be real. Dating is hard. I have tried almost every dating app. Tinder, Hinge, Bumble, you name it, and honestly, it didn’t work. I deleted dating apps two months ago to start focusing on myself and my goals. But I realized three years too late that these platforms don’t normally lead to real-life connections. […]

OPINION: USF puts the A+ in advice

Preparing for exams, a never-ending Canvas to-do list and the continuous notifications that something has been graded. This, in a nutshell, is the typical college student experience in November. It’s easy to feel alone as you check your grades and overhear your classmates’ successes. But students at USF are here to tell you this is […]

OPINION: My top picks for USF’s Roundup Comedy Show

Last Tuesday, comedian Trevor Wallace graced the Yuengling Center stage for the annual Roundup Comedy Show. Other notable comedians to visit our campus include last year’s performer Joe Gatto from Impractical Jokers, Nick Cannon in 2015 and Pete Davidson in 2017. This got me thinking. What other comedians should host our next comedy show? Related: […]

OPINION: USF has a woman president. It’s time the U.S. did too.

It’s 2024. Women are doctors, lawyers, pro-athletes and pilots, but a woman still has yet to be the President of the U.S. USF appointed its first woman president, Betty Castor, in 1994. The university is among many institutions in the country that recognizes the value of women serving in leadership roles. Related: Donald Trump’s win prompts […]

OPINION: USF students might be divided, but let’s keep things civil

As Election Day wrapped up on Tuesday, tensions were high. Throughout the country, reported threats of violence were abound. Voters anxiously awaited results throughout the night and into Wednesday. Former Republican President Donald Trump won the 2024 presidential election after he claimed the 270 electoral votes needed to win the presidency, according to the Associated […]

OPINION: It’s time to clock out USF

Fifty hours a week, no sleep and an empty stomach became my new normal. But it wasn’t always this way. I started at Tijuana Flats when I was just a freshman in college as a full-time student. It was a way to make a few extra dollars but I treated it like it was the […]